What did ESG Investors Get Out of Proxy Season 2023?

Proxy Voting is one of the most exciting aspects of sustainable investing. The idea that your investment dollars are at work effecting positive change in some of the largest companies in the world can be inspiring. Being a participant in successful campaigns that stand up to company management gives ESG investors a sense of community and purpose. It’s a huge selling point when we talk to aspiring sustainable investors.

We are currently wrapping up 2023’s Proxy Vote season. How’s it going?

Well, if you’re looking at wins, according to the helpful tracker covering the FORTUNE 250 at the Manhattan Institute’s proxymonitor.org … not so great.

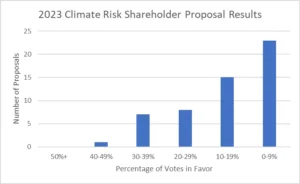

Over fifty votes on climate risk.

None passed.

In fact, only one — one! — got more than 40% of votes in favor.

Over forty votes on human rights. Zero passed.

Twenty-plus votes on Human Rights. None passed.

More than fifteen on Golden Parachutes. None passed.

7 on Civil Rights. None passed.

Shareholders went 0-for-18 at Amazon. 0-for-12 at Meta. 0-for-11 at Exxon.

Yes, some proposals get withdrawn before going to a vote, as a company and the proponent come to an agreement. But with a voting record like this, how incentivized are companies going to be to engage with proponents moving forward? Engagement is nice. Wins are better.

So, what happened?

The proposals being put forward make strong ethical and moral arguments for many of their cases. Some detail the risks involved with not fully understanding a company’s Human Rights or Climate Change exposure. But what many proposals struggle to do is win supporters with the investment case for their proposals.

The lesson of 2023 is that the investment case — a focus on fiduciary duty — is where the rubber meets the road for shareholder proposals.

And that’s a positive. A favorite slogan of ours is “ESG Investing is just Investing.” It’s looking at wider sources of potential risk, and baking that into the investment process. And this year’s votes reinforce that. Focus on the investment, and you can get the big names behind you, and you can drive real change.

This lesson isn’t new, but it’s certainly being reinforced in a big way this year. And it’s a lesson that’s been hiding in plain sight.

Remember: Engine Number 1 Set the Standard for Making the Investment Case

Nowhere has the fiduciary duty case been made better, and been better documented, than Engine Number 1’s famed shakeup of the Board of Directors at ExxonMobil in 2021.

As detailed in this excellent case study from the NYU Stern Center for Sustainable Business, Engine went full-throttle making the financial case for their cause. They made the case from a competitive point of view, showing how Exxon was falling behind the rest of the industry not just in the short term but in long-term projections as well. Their proxy statement led with this:

“Over the past decade, the Company has failed to evolve in a rapidly changing world, resulting in significant underperformance to the detriment of shareholders and risking continued long-term value destruction.”

The statement makes no mention of the Paris Climate Agreement, or the under-2-degree global warming goal. The case was made on the financials. On shareholder value. And voters listened.

When proxy advisory company ISS announced their support for Engine Number 1, they made clear why: “On the basis of operational performance alone, the dissident has made a compelling case that additional board change is needed.”

The lesson, again: Focus on fiduciary duty. Follow the money. And it’s no surprise that the big winner of this year’s proxy season did exactly that.

The Big Winner of 2023 Proxy Season: Domini Takes on Dollar General

In a field of mostly failed proposals, Domini Impact Investment’s successful proposal at Dollar General was such a statistical outlier that it’s worth noting how far they lapped the field. Outside of management-sponsored say on pay votes, and procedural proposals on voting rules and technical governance issues, there were about 350 total shareholder proposals. 4 won. A 1.1% hit rate. Three of the winners got between fifty and 52 percent of the vote. Then there was Domini’s proposal at Dollar General, which got sixty-seven percent of the votes. That’s an outlier compared to other outliers. What was the trick?

Stop me if you’ve heard this before: They focused on fiduciary duty.

In their proposal, Domini led with the money:

“Since 2017, Dollar General has received $12.3 million in Occupational Safety and Health Administration (OSHA) penalties for numerous willful, repeated, and serious workplace safety violations. OSHA designated Dollar General as a “severe violator” in 2022.”

OSHA violations are bad, but why are they bad for the bottom line? Domini draws a straight line:

“Staffing shortages and high turnover contribute to fatigue, high workload, and further exacerbate safety issues. This may also contribute to loss of new store development opportunities or poor worker retention.”

Is there even more risk going on? Absolutely, says Domini:

“Understaffing and poor security measures at Dollar General stores may also contribute to increased risk of gun violence to staff and communities. Dollar stores have become vulnerable targets for robberies, causing employees to lose their lives, according to past reports.”

Dollar General came out hard against the proposal, but their arguments were largely deflections. The company couldn’t say that they were following regulations, because they weren’t. And given the clear focus on the bottom line, on fiduciary duty, a full two-thirds of votes were cast in favor of Domini, and against Dollar General management. Fiduciary duty wins!

Similar Hopes, Different Results at Wells Fargo

The power of Fiduciary Duty was on full display at Wells Fargo this year, where there were 6 different ESG-related shareholder proposals. And one of them passed, barely, with 52% of the vote. A proposal by New York’s State and City Pension Funds asking the company to prepare an annual report on prevention of workplace harassment and discrimination. How did they eke out a win? By focusing on fiduciary duty, of course. They pointed to reports of criminal investigations at the company, tied it to fiduciary bottom-line competitive issues, and made the case of why the report would benefit shareholders.

But let’s focus on some of the climate-related proposals failed to pass at Wells Fargo, with none of them garnering more than 33% of votes, and one failing to capture even 10% of votes. And let’s see how fiduciary duty played a role in the results.

As You Sow Sets the Line

Not surprisingly, some of the highest vote-getting proposals around Climate Risk came from As You Sow, a long-time player in the shareholder engagement game and a resource that we often point to. Let’s have a look at their Wells Fargo proposal:

As You Sow asked for more details from Wells Fargo in how they were going to meet their own stated goals for emissions reduction. As You Sow made the strong case that while Wells Fargo had made commitments to reduce fossil fuel investments by 2030, they had actually increased their fossil fuel funding since 2019 — the largest company to do so. It was a compelling case to be sure, and in terms of effectiveness of a proposal that asks a company to put out a report of this kind, it did as well as could be expected. It garnered about a third of all votes, which is far better than many other ESG Climate Risk proposals.

But still — why only a third of voters, when climate risk is such an important issue?

What the As You Sow proposal didn’t do was make clear how shareholders were going to benefit from Wells Fargo issuing the report publicly. If Wells Fargo was meeting all regulatory requirements and industry best practices — and they were — it wasn’t then clear why the company should have to publicly disclose additional information compared to its competitors. In its response, Wells Fargo said exactly that:

“We believe Wells Fargo’s existing work developing transition plans in line with evolving market practices remains the prudent approach, and we do not believe that producing the report required by the proposal would ultimately serve the best interests of our shareholders.”

And in the end, the majority of shareholders agreed with the company.

This isn’t to say that the As You Sow proposal was a waste of effort — it made a strong case and it’s good to know that a strong case on its own can get a third of voters. It’s something to build from, and Wells Fargo management has to consider that a significant amount of shareholders. As You Sow saw similar positive results at JP Morgan, Bank of America, and Goldman Sachs.

In addition, As You Sow also reached agreements and withdrew proposals at companies like John Deere, Morgan Stanley, and others. Surely their reputation of getting shareholder support helped their causes there.

On the other hand, some proposals fared so poorly it’s hard to see where to go from here.

Sierra Club Stands Nearly Alone

The same Wells Fargo shareholders that passed the workplace harassment proposal and rewarded As You Sow’s strong proposal with a third of votes, only gave 8% of votes to another climate-change related proposal from the Sierra Club. What went wrong?

The proposal asked Wells Fargo to create a “time-bound phase out” of the company’s loans to the fossil fuel industry. While this is a noble goal, the reality on the ground is that Sierra Club was asking Wells Fargo to phase out a very legal, and very profitable business. The case for fiduciary duty was simply not being made. In fact, rather than making their case based on fiduciary duty, these proposals were asking for support in lieu of fiduciary duty. Similar Sierra Club proposals at Bank of America and Citigroup failed to cross the 10% threshold. A proposal at Morgan Stanley got less than 5% of votes. That number is particularly painful — getting under 5% of votes means the topic can’t be re-filed.

This is not to call out Sierra Club specifically — 38 of the 55 Climate Risk shareholder proposals in the ProxyMonitor database failed to garner even 20% of votes. The chart below doesn’t exactly inspire. Yes there are a lot of proposals. The question is — to what end?

Mainstream shareholders are making their voices heard loudly: Proposing something that is bad for the short- and medium-term bottom line of the company, clearly, is not getting traction.

Faring Worse than ESG: Anti-ESG

While pro-ESG proposals struggled in the wins category, anti-ESG proposals did demonstrably worse. The conservative National Center for Public Policy Research laid out over 20 proposals, including contesting DEI practices at McDonald’s and Walmart, and challenging FirstEnergy’s Net-Zero goals. With a few votes outstanding, the Center’s proposals have gotten an average of about 2% of votes so far.

Two percent! And yet we are having major discussions on Capitol Hill and in state legislatures across the country about anti-ESG regulations. Maybe — just maybe — those discussions don’t reflect the opinions of the populace? Anyhow.

Applying Lessons: How Can Proponents Deliver Wins in 2024?

So if the big lesson here is on fiduciary duty, how can proponents deliver more wins to ESG investors next year? A few thoughts:

- Follow the news — and the fines. Domini and the New York Pension Funds both made successful cases based on fines or criminal investigations that properly spurred voters to act. A successful proposal regarding Employee Rights at Starbucks did the same. So who’s in the news for fines lately? McDonald’s is, for child labor law violations. Meta has been hit with record fines from the EU on data privacy issues. Might shareholders benefit from additional reporting on how company management is addressing these issues moving forward? They might!

- Think like an investor. Remember that line — “ESG Investing is just investing.” So, where could ESG investors use more/better data? One big headline recently was that some insurers are pulling out of California due to increased wildfire risk. As an investor, I’d like to know how much of an insurance company’s business is drawn from areas that are under increased risk of losses due to climate change. That would help me evaluate the value and risk profile of the business going forward. As Larry Fink has said, “climate risk is investment risk” — so find the industries where that risk is most prevalent, and take the fight there.

- Attention can be costly — so pick your spots. If you’re not making your case on fiduciary duty, voters have been very clear this year that they won’t vote for your proposal. While it’s understood that sometimes the vote isn’t the point — that publicity is important as well — at some point a loss is so big that it can be used against the proponent to show that they are out of touch. If you’re going to stick your neck out there, make sure there’s good that will come from it.

We have reached the point in the evolution of ESG proxy voting has been identified as a significant tool, but diluting the field may end up doing more harm than good and discourage potential ESG investors. When only a small fraction of proposals get any traction, at some point, ESG proponents are going to stop getting attention. In 2024, the focus should be on quality over quantity, bumping that win rate, and driving real change rather than making a poorly-supported point.