Silicon Valley Bank: ‘Wokeness’ or Just Bad Governance? An ESG Analysis

When Silicon Valley Bank (SVB) collapsed last week, it sent panic signals throughout the market. And for reasons that aren’t clear to us, some of those panicked voices started blaming “wokeness” for the failure. But how accurate is that critique? If you did a deep dive ESG (environmental, social, and governance) analysis of SVB, what would it have shown?

For a certain segment of our political discourse, wokeness has become a criticism to hurl at sustainable investing in general, and ESG analysis in particular. But it’s a strange criticism. ESG isn’t a political assessment, it’s a way of identifying long-term risk factors at a company and seeing how the company is managing that risk.

So, let’s put our ESG Analyst hats on, rewind a few months, and ask the ESG question — how is SVB doing with managing its long-term risk?

MATERIAL = RISKS THAT MATTER

The first thing we need to do in our analysis is to figure out what risks are most material for a bank like SVB. Material, in this case, means most likely to have an impact on the operations, and therefore the valuation, of a company.

Luckily there is a great, publicly-available tool to help us do so. The SASB Materiality Map has become an industry standard for identifying the issues that are most material for a particular industry — as in, those that are most likely to affect the company’s bottom line.

For commercial banks like SVB, SASB identifies five material issues:

- Data Security

- Financial Inclusion and Capacity Building

- Incorporation of ESG Factors in Credit Analysis

- Business Ethics

- Systemic Risk Management

Notice that this list doesn’t focus on environmental issues like greenhouse gas emissions, or social issues like diversity. It’s a very governance-oriented list, because ultimately that’s what matters to a bank. Each of these areas, according to SASB, are places where a bank like SVB should have strong guardrails in place so that they don’t cause harm to customers, regulators, or other stakeholders.

Once you know what the material risks are, the next question is whether a company is transparent and honest in reporting about those risks. For each of these material issues, SASB has recommendations for what a company should disclose so that analysts can see how they are doing. In this case, SASB recommends disclosing the following:

1. Global Systemically Important Bank (G-SIB) score, by category.

This is a score established by an international body that monitors the global financial system. It looks at if banks are “too big to fail.”

2. Description of approach to incorporation of results of mandatory and voluntary stress tests into capital adequacy planning, long-term corporate strategy, and other business activities.

The key phrase in this word salad is “stress tests.” Stress tests are mathematical models that demonstrate how a bank would respond to major risks in the market or economy. For example, rising interest rates are always a pain point for banks — what would happen if rates rose dramatically in a short time? This disclosure is about demonstrating a company’s commitment to doing rigorous stress testing and how they respond to the results.

ESG ANALYSIS — SVB VS KEYCORP

So, let’s take a look at how SVB does in an ESG review. And to compare, let’s also look at another regional bank, KeyCorp.

Both SVB and KeyCorp report “SASB Indexes,” which is pretty impressive! SASB-related disclosures are not required by regulators, nobody is forcing them to do this. Here’s SVB’s, and here’s KeyCorp’s. Both of them say that they do not have G-SIB Scores because of their size. And, both of them say to look to their 10-ks to see their approach to stress-testing.

So, here’s SVB’s 10-k, and here’s KeyCorp’s. Let’s start with KeyCorp.

KeyCorp talks quite a bit about stress testing, and the role of their Market Risk Management (MRM) group in performing and monitoring that testing:

Let’s compare that to what SVB has to say about stress testing, who runs it, and how it is used.

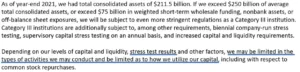

At the bottom of a section called “Capital Resources,” they mention their testing.

It is clear that SVB knows what a stress test is … but do they actually take it seriously? It sure sounds like they only do them annually. Later, they mention that they have their own ALCO:

Again, it is good to know that they do some stress testing, but there’s no detail on the rigor involved.

MORE ESG INSIGHTS ABOUT SVB

In fact, the place where SVB spends the most time talking about stress testing is when discussing their total assets. That’s because they were getting close to a threshold that would expose them to higher regulations. Look at how they discuss this:

Did you catch that? What they are saying is that if they have to do more rigorous stress tests, they might not be able to conduct business as usual. The risk, in their mind, is that such stress tests might indicate they are managing their risk poorly. It suggests that they knew they were poorly managing risk, and didn’t want to have that exposed. That lawsuit is going to be interesting.

ESG: TOUGH QUESTIONS ABOUT REAL CONCERNS

Let’s review what we’ve learned as ESG analysts. We have seen that KeyCorp is prepared to talk, transparently and at length, about stress testing and how it is used in risk management. We can’t see the results, but we know that the process is in place.

And we see that SVB doesn’t provide much transparency, and in fact appears to be hesitant to do real stress testing. There may be a process in place, but we can’t see much evidence of it.

ESG analysis would suggest the following: if a company cannot, or will not, discuss material risks in detail, in a public forum, what does that say about the firm’s approach to those risks? If you’re an investor, or even a customer at the bank, it only seems reasonable to ask some tougher questions.

That is the power that ESG offers. As an ESG analyst in the fall of 2022, we would wonder if SVB was managing their long-term risk well compared to their competitors. We would incorporate that into our overall evaluation of the company. We might well bring our assessment of the bank’s valuation down as a result. If we are investing for the long-term, there were signs that SVB might not be a great bet.

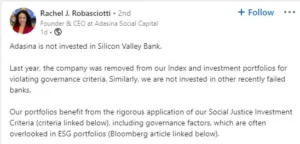

And boy would that have been the right move! It’s why you can see LinkedIn posts like this:

THAT is ESG at work. That is managing long-term risk, seeing a potential disaster, and steering your money into safer investments. Done right, ESG is asking the right questions about what’s material, what’s financially relevant, and if a company doesn’t have a great answer, moving away.

Don’t worry, though. According to their ESG report, SVB is going a great job of counting their greenhouse gas emissions! And they … enjoy hiking?